Statistics and trends would back the creation of the Super Metropolitan Centre Zone

As I prepare for my final Unitary Plan hearing tomorrow in Manukau (on Manukau) I came across evidence from a big submitter (AMP Capital Investors NZ Ltd and PSPIB Waiheke Inc) who own the Manukau Supa Centre site (which is west of the Metropolitan Centre Zone for Manukau).

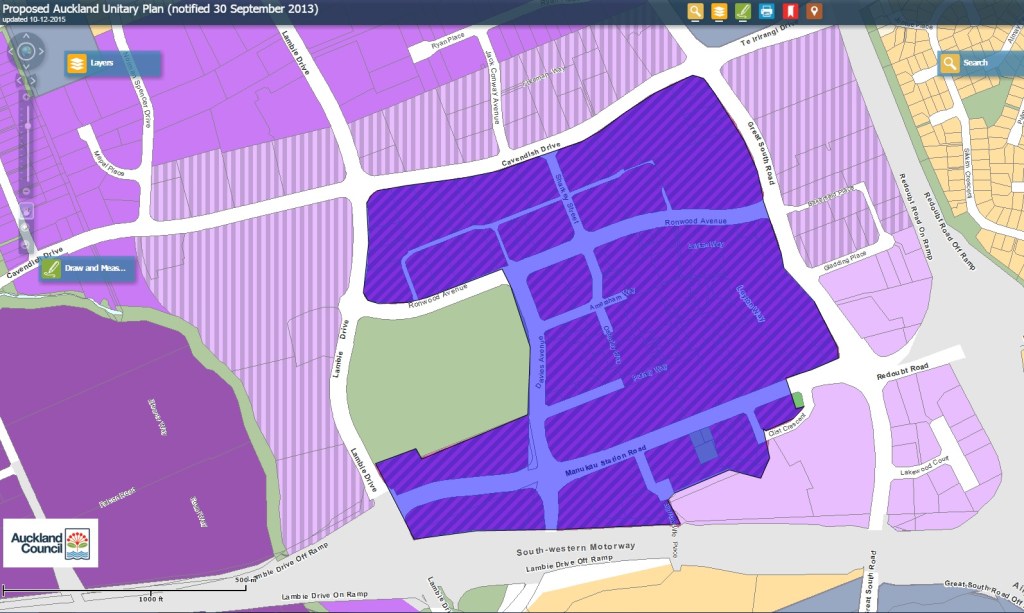

The current zoning for the Manukau Supa Centre site (as well as where Harvey Norman, Bunnings and Mitre 10 are also located next door) is General Business Zone with the Heavy Industry Zone applied next to that further west. Now the Council has said this area is General Business Zoned as it acts as a buffer between the Heavy Industry Zone and the Manukau Metropolitan Centre Zone. However, as the evidence will show from AMP et al is that if the Heavy Industry Zone to the west and up to Plunket Avenue is flipped to Light Industry Zone then the General Business Zone to the west of the Manukau Metropolitan Centre zoned area can also be extended to Metropolitan as well.

This would mean if the Unitary Plan Hearings Panel allows the extension of the Manukau Metropolitan Centre westward the following would happen:

- Land mass wise Manukau moves from 45.83 hectares (third biggest behind Albany and Henderson Metropolitan Centres) to second at 62.68ha (behind Albany at 69.02ha)

- In terms of current Gross Floor Area (of existing buildings) goes from 86,500m2 (second largest behind Albany’s 148,100m2) to 152,100m2 or the biggest of all the Metropolitan Centres in Auckland

Source:

Given Manukau is also connected by following transport links below the above figures are quite formidable:

- State Highways 1 and 20

- Great South Road, Cavendish Drive, Redoubt Road, Wiri Station Road, Lambie Drive and Te Irirangi Drive

- Nexus point for South Auckland buses

- Manukau Rail Station

- Some cycle lanes

It also means Manukau and Albany would be the largest two Metropolitan Centre zoned areas in Auckland (no other Metro Centre gets above 87,000m2 or 60ha) serving the largest catchments outside of the City Centre itself.

So what does this mean?

Below is the evidence and supplementary evidence from AMP Capital Investors NZ Ltd and PSPIB Waiheke Inc on expanding the Manukau Metropolitan Centre zone:

Key extracts from the Evidence:

1.5: Office, retail and community services are integral to the Manukau City Centre and, on the basis of the Business Land Report, demand for floorspace for these activities will grow faster than any other activities. The Business Land Report reinforces my view that floorspace demand in the Manukau catchment will be greater than projected and needs to be adequately provided for.

1.6: Intensity of development directly addresses the issue of realisable supply. While office and residential activities can be accommodated in floorspace above ground floor, intensification of retail realistically will require greater ground level floorspace, which means higher cover ratios or greater centre area. From my analysis of vacant or vacant potential land in the Manukau Metropolitan Centre zone I conclude that there is a need to expand the centre area to accommodate the projected retail demand

1.10: The location of retail activities can have a major impact on urban form. The location and success of retail is critical to the vitality and viability of a centre. A concentration of retail activities within a centre provides a platform to encourage other service activities, community facilities, and professional offices. A centre that has high amenity encourages the establishment of visitor accommodation and residential development within and in proximity to the centre.

1.11 In Manukau, the retail offering is primarily located in the Metropolitan Centre zone (approximately 60%) and the Manukau Supa Centa and adjoining business land (Site) (approximately 40%).

1.12: These two significant retail areas are located at either end of the central city area, with the concentration of civic services, office development, key public transport infrastructure (notably the train station), and public open space (Hayman Park), lying between these retail centres.

1.17: My evidence has assessed the retail demand projected from the population growth in the Manukau and Papakura catchments, and compared this to the retail floorspace capacity, and realisable supply, in the Metropolitan Centre zone.

1.18: Although there is sufficient retail floorspace capacity to meet demand, I consider that the realisable supply in the Metropolitan Centre zone is not sufficient to meet demand.

1.19: This will lead to retail activities establishing outside of the Metropolitan Centre zone. This is likely to result in retail development becoming more dispersed within the business zones surrounding the Metropolitan Centre, or locating further away from the centre.

C. MANUKAU CITY CENTRE

1.23: Manukau City Centre is the retail and commercial hub of South Auckland. Auckland Council’s analysis confirms that it is one of the largest retail hubs (by retail floorspace), and the second largest centre of employment in Auckland. There are parallels to be drawn between Albany in the north, and Manukau to the south, which I will refer to in my evidence.

1.24: Considerable investment has been made in Manukau City Centre to create public infrastructure that effectively services the commercial, community and governance requirements of a major sub-regional centre. This includes the development of extensive transport links and services (road and rail), recreational parks, and welfare facilities (including the district court and police station).

1.25: Manukau City Centre is the closest major centre for 186,000 people (13% of Auckland’s population). Auckland City has ten Metropolitan Centres, therefore Manukau already needs to service more than its fair share of Auckland’s existing population.

1.29: In my view, the attractiveness of Manukau City Centre is relatively high in respect of location and amenity but low in respect of retail offering (particularly in comparison retail) compared with its neighbours in Botany and Sylvia Park.

1.30: Manukau City Centre contains around 152,100m2 of existing retail floorspace (which is comparable to Albany Metropolitan Centre of 148,100m2). Manukau City Centre provides 50,700m2 (33%) of SFR (almost all in the existing Metropolitan Centre zone), and around 101,400m2 (67%) of LFR (62,800m2 within the Site and 38,600m2 in the existing Metropolitan Centre zone).

1.37: I have also identified that within the Metropolitan Centre zone there is currently limited visitor accommodation, and no significant residential accommodation. There are very few vacant or vacant potential sites within the Metropolitan Centre zone to facilitate this type of development. Increasing residential and visitor accommodation within Manukau City Centre, and in particular enabling it to occur on the Site, will enhance the vitality and amenity of the centre for the benefit of local businesses, customers and the wider community.

D. RETAIL DEMAND AND SUPPLY

Population Growth

1.40: The Manukau and Papakura catchments are projected to have significant population growth to 2031 (an increase of 28% (medium) or 43% (high) compared to current household numbers).

1.41: In my view the medium growth scenario is the most likely and appropriate to use for long term planning. However, I also believe that the Council’s growth rate projections underestimate the growth in the short to medium term. My adjusted projections show 10,000 new households compared to the Council’s 6,000 new households by 2018.

1.42: Current indications of the cost of house construction and market sales in Manukau and Papakura also make it likely that new households in these areas will enjoy higher incomes than existing households in these catchments. This will increase household spend available in the catchment relatively faster than has been the pattern to date.

1.43: The growth in population will lead to a greater demand for goods and services. This demand is an opportunity to provide further commercial intensification in Manukau City Centre.

Retail Demand

1.44: I have applied Auckland Council’s “base case” estimates of future demand in Manukau Central derived from household growth which show it will support 95,400m2 additional floorspace, of which non-trade retail is estimated to be 78,400m2 (including 60,700m2 of “core retail”)3. The Manukau Central area [confirm the area this covers].

1.45: Auckland Council’s modelling also shows that Manukau Central has the greatest potential growth in demand for retail floorspace (out to 2031) of any of the City’s sub-regional areas (eg. in comparison growth in demand in the Albany catchment is projected to be around 61% (47,900m2 floorspace) of the growth in Manukau Central).

1.46: In my view demand for retail floorspace in Manukau Central will be slightly greater than projected by the Council out to 2020-2021, and possibly beyond, on the basis of my greater growth rate projection in the short to medium, and the higher household income of new residents.

1.47: Taking into account the higher household growth (but not higher household income), I estimate that the projected retail demand for additional core retail floorspace in Manukau Central over the 2015-18 period is 11,900 m2. This is 34% higher than the 8,900 m2 of growth under the (Council’s) constant growth profile projection.

1.48: In my view it may well be that retail demand will remain stronger beyond the 2018 term. This is because more land is likely to P1152_15699_043.docx 10

become available in South Auckland for residential development through implementation of the Future Urban Land Supply Strategy (FULSS).

1.49: To meet the projected retail demand of 95,400m2 (by 2031) at current levels of sales performance is equivalent to adding around 60-65% to the existing supply in the combined Metropolitan Centre zone and Site over the next sixteen years.

1.50: If this retail demand was only to be accommodated within the Metropolitan Centre zone it would be the equivalent of adding around 108% to existing supply (or more than doubling existing supply) over the same sixteen year time period.

E. BENEFITS OF REZONING THE SITE TO METROPOLITAN CENTRE

1.71: Overall I consider that there are significantly greater positive economic effects from rezoning to Metropolitan Centre and enabling a wider range of activities and intensification on the Site, including:

a) improved attractiveness of the Manukau City Centre thereby drawing more consumers and reducing spending leakage out of the Manukau catchment (preferably increasing the 69% household spend rate within the Manukau catchment);

b) advantages of increased competition from a broader retail offering;

c) improved ability for business to respond to the market as a result of improved services within the centre, greater buying power to enlarge product ranges, better access to the labour market as a result of the growth of the local population;

d) improved amenity in the Manukau City Centre as a result of a broader range of activities on the Site, including core retail, offices, residential and visitor accommodation, services and community facilities;

e) agglomeration benefits from consolidation and greater intensification of retail, office, community and social services;

f) more jobs in the Manukau catchment; and

g) more certainty and lower resource costs for development within the Site.

—————————

In short if you combine the above with my own Super Metropolitan Centre evidence it demonstrates that Council is again short changing one of its two biggest Metropolitan Centres – Manukau (the other being Albany) at least in the planning department. We know Panuku Development Auckland are due back next week to the Auckland Development Committee with their High Level Project Plan that marks the official start of the Manukau Transform program by them.

But as shown in paragraph 1.74 above if Panuku are to achieve maximum bang for public dollar buck then we need to achieve that critical mass with Manukau City Centre starting with the planning regime. So extending the Metropolitan Centre zone to cover the Manukau Supa Centre site (currently General Business Zone) then flipping that to the Super Metropolitan Centre proposed zone would go a long way in achieving that paragraph 1.74 from AMP Capital et al.

Rezoning Primary Evidence

Supplementary Evidence