Compiling Auckland’s growth issues along with Government’s debt issues

I am going to compile both my #Budget2017 Lacks Vision for Auckland. So I Crunch Some Numbers and State Infrastructure Banks and Housing – Take 2 along with this post from the AUT’s Briefing Papers’ Public Debt: How Low Should It Go? to form a more complete long read on the issues facing Auckland and how Government is not exactly helping in all that it can.

With the elections on September 23 it is yet what the Government will do to try to win over the 34% of the vote the Auckland bloc makes up and stave off challenges from the Opposition especially the Greens. Remember only about a 4% swing in the vote against National is needed to bring in a Labour-Green led Government.

Source: http://thespinoff.co.nz/28-01-2016/a-brief-history-of-national-mps-trashing-the-rail-link-they-just-funded/

The story on Budget 2017, Auckland’s Growth and support it needs, and how Government is allergic to using the primary tool to support that growth in Auckland – DEBT:

#Budget2017 Lacks Vision for Auckland. So I Crunch Some Numbers

Nothing for our Major City

I can understand this article entirely (Average family: ‘You get quite despondent even reading Budgets’) given Finance Minister did not exactly announce anything new or of worth to alleviate the current pressures Auckland faces. But I am going to take this one step further and look at what a Policy for Auckland could be to help relieve pressures, not break the bank, and actually give a true tax cut.

I am going run some numbers through this post followed by stitching it up at the end.

The numbers with Auckland

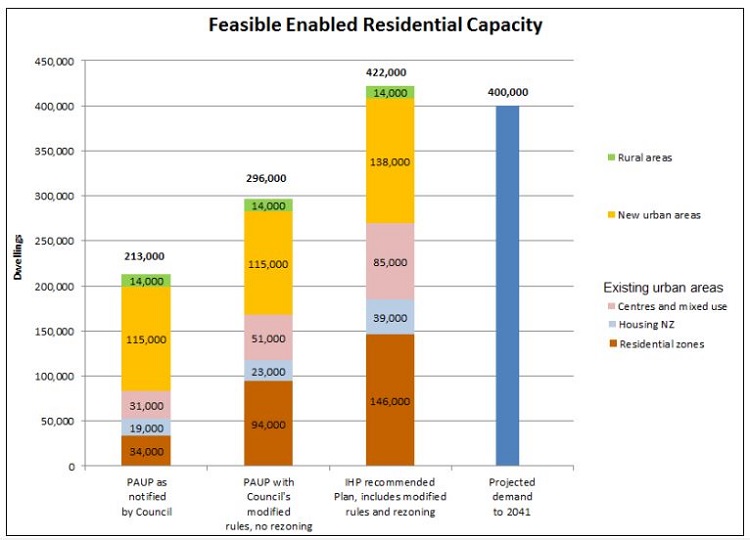

Growth and Housing Projections under the Auckland and Unitary Plans

- 780 new residents a week X 52 weeks = ~40,560 new residents a year to Auckland

- Unitary Plan has capacity for 422,000 dwellings over 30 years or 14,066 dwelling to be built a year if on a linear path

Housing Needs to nominal population growth mentioned above

- 40,560 new residents a year

- Working on assumption of average three people to a dwelling

- 40,560 / 3 = 13,520 homes a year (so just under Unitary Plan annual theoretical capacity)

- The above does not factor in the 40,000 dwelling deficit already in place in Auckland. So to get them up first requires a 2.85 year dwelling build at the 14,066/year build I have set using the Unitary Plan numbers

Southern Auckland Future Urban Zone and Transform Manukau Yields

- Transform Manukau has forecast an extra 20,000 new residents meaning 6,667 new dwellings required

- Southern Future Urban Zone has capacity for ~55,000 new residents and 35,000 new jobs (this does not include expansion of the Wiri or Airport industrial complexes)

- 55,000 new residents = 18,333 new homes

- Not including other developments in Brownfield areas in Southern Auckland that means 75,000 new residents and 25,000 new homes at minimum

Totals

- 40,000 new homes needed to get on top of current deficit

- 25,000 new homes for new residents above and beyond the deficit

- 65,000 new homes taking around five years if building to full Unitary Plan capacity yields

Your policy is around the 65,000 new homes over five years (with 25,000 new builds in Southern Auckland), laying down the foundation for industry and commerce to build and provide subsequently 35,000 jobs and then stitching it up with a transport system. The numbers I have given are the bare minimum in keeping Auckland afloat in terms of providing housing, land for employment growth and a transport system linking the two up. Budget 2017 did nothing to execute such a policy above, the policy being Growing Auckland.

As for transport to stitch up Southern Auckland to the rest of Auckland? Pukekohe Electrification and an interim busway from Manukau to the Airport certainly would not go amiss.

Cost to execute the policy? $4.25b conservative, figure will be higher if the Government increases the percentage of it building the 65,000 new homes over the private sector.

The cost to ignore the policy? The Treasury Benches post September 23.

…….

So $4.25b needed just to get Southern Auckland set up to take the initial brunt of Auckland’s continued growth. How to fund it in the most equitable manner available? The State Infrastructure Bank:

State Infrastructure Banks and Housing – Take 2

How the Government can lower development costs

Housing and Government debt seem to be ignored by the Budget and pundits alike. Why when the two are linked I don’t know but it comes down to managing verses leading when it comes to an acute situation such as the housing shortage in Auckland.

Right now inflation, the Official Cash Rate (that governs interest and Bond rates) and 90 Day Bills (Short term bonds) are all rather low while Real GDP growth is not getting above 1% (Real GDP unlike Nominal GDP factors in both inflation and population growth). This means wages are stagnant, productivity and growth bombs and for some reason we have a Government allergic to using debt instruments to move things along. Furthermore this Government is trying obtain Budget Surpluses which is a fiscal contraction policy tool designed to take money out of the economy and prevent it from overheating. You normally run surpluses when inflation and the Official Cash Rate are both high – of which both are neither. On the flip side Budget deficits are a fiscal expansion tool to pump money into the economy to stimulate it. Normally the deficits would be used to fund infrastructure to set up support for the next boom. Once the boom is underway with inflation, Interest Rates and wage growth creeping up do you then switched to Balanced Budgets (steady as she goes) then Surplus to act as the break if things overheat beyond a Balanced Budget.

Now where am I going with this?

Well as I said earlier our key indicators are low but the Government is trying to run a Fiscal Contraction policy. In the meantime Auckland is under high population growth and does not have the housing or infrastructure to support the new residents we are getting (780/week). To make matters compounded Council is at its debt limit to fund new infrastructure like water while conventional Development Contributions from developers when building new homes have the double effect of not fully paying for new infrastructure needs AND due to the upfront nature of Contributions add a significant portion to the new house price. The ultimate consequence? Stalled infrastructure developments with steep upfront Development Contributions bearing on the final house price as Council tries to get infrastructure investment going again.

Government funds infrastructure

How we fund water, civic amenities and even transit will need to change. Development Contributions all upfront are simply not working, not when you have the nation’s largest money handler sitting right in front of you – that being The State! Given the State can access currency and credit at Rates cheaper than any private institution the State is in the best position to bankroll infrastructure funding.

Thus a State Infrastructure Bank would be set up and loan money to Councils to get the infrastructure built. The term of the loan is 50 years at nominal interest and is repaid as a Targeted Rate on property or properties affected by the new infrastructure to Council who then pays it back to the State Infrastructure Bank. The new infrastructure cost is spread via the Rate applied to the property over 50 years rather than a full upfront cost via the conventional Development Contribution. Regional infrastructure such as motorways or heavy rail should be born by the National Land Transport Fund thus all taxpayers given the often national benefits by such infrastructure (where as Light Rail would be borne by the SIB targeted Rate system).

With Development Contributions thus the upfront cost taken off the price of a new build and shifted to a Targeted Rate on the affected property over 50 years hopefully both house prices can stabilise out (and more affordable for smaller builds) while infrastructure is built.

What could the SIB loan money on? Well got a few ideas here at the price of a couple of billion dollars – #Budget2017 Lacks Vision for Auckland. So I Crunch Some Numbers

Of course there are more finer financial intricacies to a State Infrastructure Bank and how much of a percentage it should bank roll non regional transport infrastructure (heavy rail and State Highways) and so on but hopefully by penning down the basics here something might get rolling. Because the current method through Council debt and Development Contributions is simply not working while terms of finance are very favourable for Budget Deficits to fund the State Infrastructure Bank.

In the end the State needs to intervene in a broken system.

Thoughts?

…..

An extract from The Briefing Papers on Government’s allergic reaction to debt and how that has hamstrung Auckland:

Public Debt: How Low Should It Go?

I asked him [Keynes] if he would borrow if he were in New Zealand in order to get through the crisis. Keynes replied, ‘Yes, certainly if I were you I would borrow if I could, but if you asked me as a lender I doubt whether I would lend to you.’

(Diary of the Minister of Finance Downie Stewart, 1932)

The history of the New Zealand economy is riddled with borrowing crises in which offshore over-borrowing was followed by the tap being turned off; New Zealand then experiencing cold turkey with its ugly domestic consequences. It is not something which is at the forefront of the public’s thinking, but it is an ongoing concern to Treasury and the Reserve Bank officials. They are regularly reminded of it by the reviews of credit-rating agencies, who are going through the same process publicly as our big lenders do privately.

As a result, there is an ongoing quest for measures that reduce New Zealand’s exposure to foreign debt. For example, in the 1980s it was announced that the government would not (usually) borrow overseas, but only domestically. But private New Zealand was allowed to borrow overseas virtually without restriction.

This strategy was assumed to insulate the government from foreign borrowing. A standard neo-liberal analysis was that private transactions were nothing to do with the government but were the responsibility of the foreign lender and the private New Zealand borrower.

Faced by the Global Financial Crisis, the theory collapsed. The New Zealand government found itself exposed to bailing out the financial sector (which was the main channel of the foreign borrowing) both as finance companies failed and as trading banks faced an international liquidity crisis. Fortunately, measures had been already taken to prepare for the management of such crises, and world liquidity did not really jam up. But this memory has been added to a number of earlier borrowing crises.

The high private international debt that New Zealand carries is why the credit rating agencies are cautious about the level of public debt which, as we shall see, is low by international standards. I understand that when they draw attention to it on a visit, our officials who understand the problem as well as the agencies are always a little uncomfortable.

One measure is to keep the New Zealand government’s debt to a low level (even though it is domestically denominated). The 2017 budget promises to reduce it even further.

Definitions of outstanding public debt are complicated. The OECD provides ‘General Government Gross Financial Liabilities as a Percentage of GDP’. ‘Gross’ may mean there are some offsetting assets such as foreign exchange reserves; ‘general’ includes levels of government below central government. For 2015, the latest year available, the New Zealand ratio is 38.1 percent compared to the OECD average of 111.2 percent. Only Australia and Estonia are lower.

……

Source and full article: http://briefingpapers.co.nz/public-debt-how-low-should-it-go/

A rather bad mix of: lax immigration policy, major population growth in Auckland, infrastructure previously under-invested in Auckland, the double whammy of catching up with that infrastructure-deficit let alone new infrastructure for the future growth trends, and a Government not willing to use its Sovereign Powers and Currency to help essentially a mess of its own making in Auckland. The perfect storm you could say.

September 23 and the people might get restless